The Kiwi dream is DEAD! I’m from New Zealand, where owning a 3-bedroom house on a quarter-acre section used to be the norm—our birthright, something to strive for. But with skyrocketing home prices, that dream is slipping away for many. And it’s not just a New Zealand problem—Australians, Americans, and Brits are facing the same challenge. Buying a big house with a big backyard was once a blessing, but today, it could be holding us back.

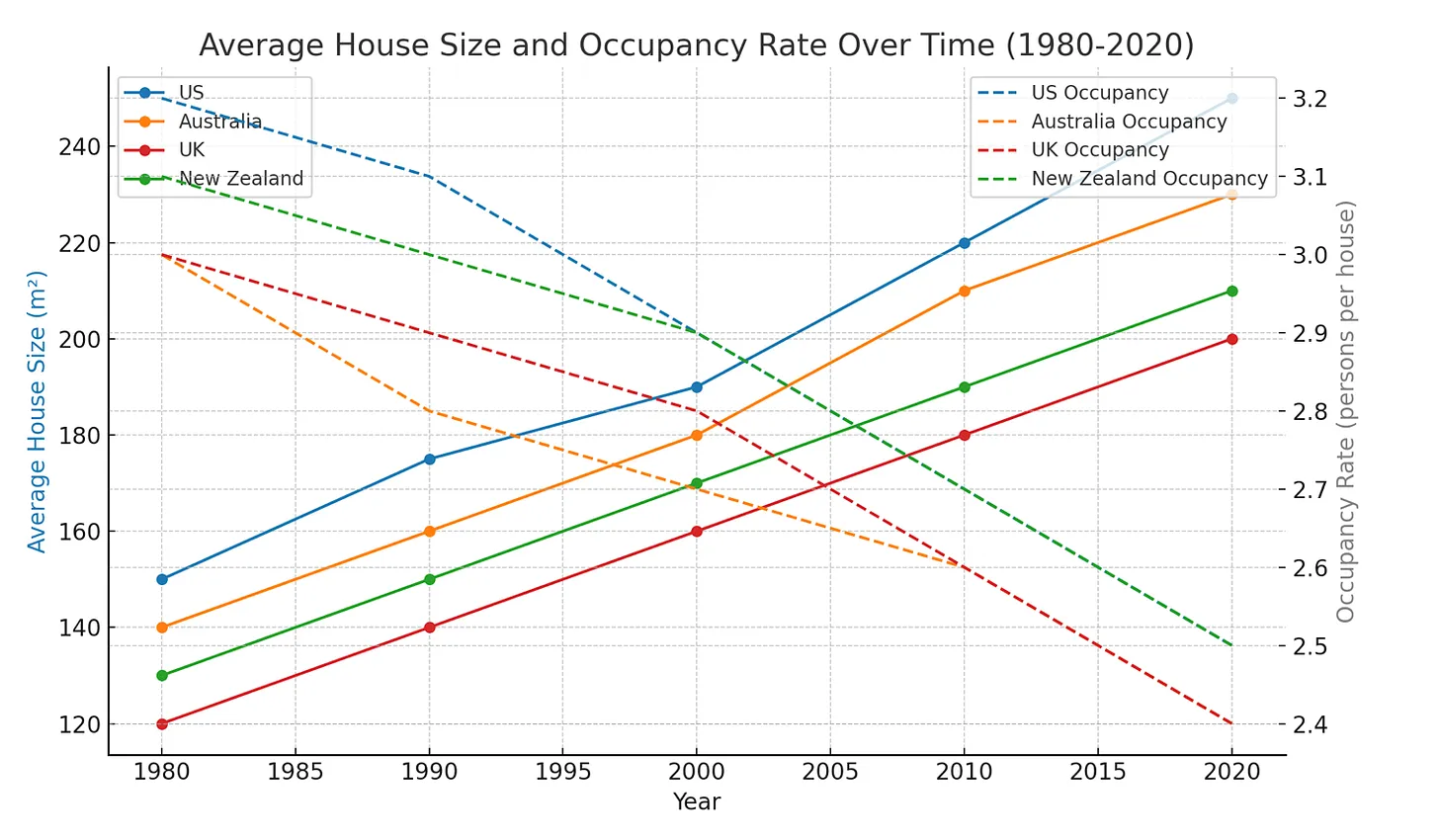

Owning a home is a dream for many, but buying bigger than we need comes with serious costs. In places like the US, Australia, the UK, and New Zealand, people often stretch themselves to buy homes far larger than necessary. The financial opportunity costs of doing this could prevent us from building wealth or retiring earlier. It’s time to rethink whether bigger is always better when it comes to homeownership.

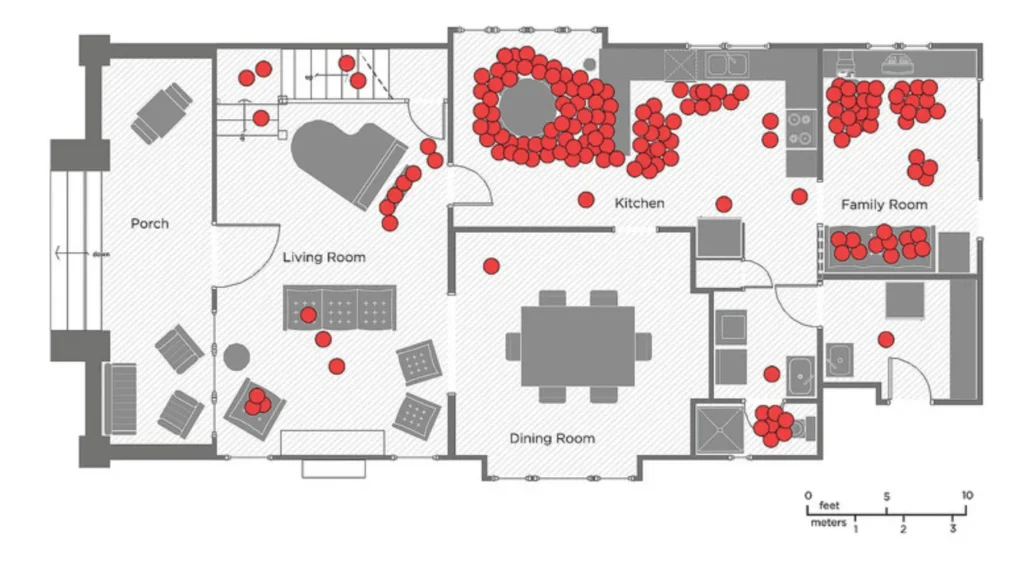

The HeatMap above is from a US study. The study examined 32 middle-class families over the course of four years – 2014, 2015, 2016, and 2017 respectively. A part of this study monitored and collected data on where in the home people spend the majority of their time. The results are fascinating. Look at all that unused space. What areas of your home would be missing red dots? Worth thinking about.

When you compare the median house price in each country to the percentage of unused space, the costs of this inefficiency are eye watering:

– US: $147,000 AUD spent on unused space.

– Australia: $228,030 AUD spent on unused space.

– UK: $138,300 AUD spent on unused space.

– New Zealand: $238,095 AUD spent on unused space.

These figures represent money locked up in bricks and mortar that could have been invested elsewhere. Instead, it could have been used to retire decades earlier or to work part-time and travel more. These numbers reflect lost time—time spent working to pay off something you didn’t even need in the first place. It’s a real tragedy when you think about it.

Instead of spending on unused square footage, homeowners could invest that money. For instance, by diverting the cost of unused space into an ETF like Australia’s VAS ETF, which has an average annual return of 9%, homeowners could generate significant wealth over 30 years:

– US: $1.98 million AUD.

– Australia: $3.07 million AUD.

– UK: $1.86 million AUD.

– New Zealand: $3.19 million AUD.

This illustrates the true cost of buying a house that’s too large—not just the direct financial expense, but also the lost opportunity to grow wealth and achieve financial independence. Beyond the financial benefits, the money saved could have been used to take extended time off work to travel, volunteer, or pursue whatever you’re passionate about. The key takeaway is that by rethinking our approach to buying a home, we can create more time for the things that truly matter. And if you ask me, time is the ultimate form of wealth.

Despite the financial downsides, there are valid reasons why people opt for bigger houses. For many, a larger home is seen as a symbol of success and achievement. The desire for more space can stem from societal pressures, a desire for a higher standard of living, or the belief that a bigger home offers greater comfort and security. Additionally, some view it as an investment for the future, hoping it will appreciate in value or provide room for family growth. Ultimately, the decision is often driven by personal aspirations, societal expectations, or the belief that a larger home equates to a better quality of life.

Benefits of Buying a Smaller Home

For those willing to downsize or buy a smaller home, the financial and lifestyle benefits can be substantial. Smaller homes typically mean lower mortgage payments, reduced insurance cost, property taxes, and smaller utility bills, freeing up cash that can be invested, spent on travel, or put towards other personal goals. With less space, there’s also less clutter, fewer chores, and lower maintenance costs, contributing to a simpler, more streamlined lifestyle. Most importantly, the savings from purchasing a smaller home can accelerate your path to financial independence and even help you retire earlier.

– Growing Families: If you plan to have multiple children or care for relatives, more space can provide comfort.

– Work-from-Home Professionals: Extra rooms can be converted into home offices.

– Social Butterflies: Those who entertain frequently may value the space for guests.

The Cost: For these homeowners, the financial sacrifice might be worth it. However, it’s crucial to balance current needs with long-term financial goals.

Who Should Consider a Smaller Home?

– Minimalists: If you value simplicity and lower living costs, a smaller home is ideal.

– Investors: Those focused on building wealth and retiring early can redirect savings into high-return investments.

– Empty Nesters: Families with grown children often no longer need large spaces.

The Benefits: By purchasing a smaller home, you could reduce financial stress, achieve financial independence faster, and enjoy the flexibility of having extra funds for other pursuits.

Buying a home is one of the most significant financial decisions you’ll ever make. While a larger house may seem tempting, it often comes with wasted space and soaring costs that could be better invested elsewhere. A smaller home not only allows you to save and invest more effectively, but it also puts you on the path to achieving your long-term goals, like early retirement and financial freedom.

At the end of the day, the right choice comes down to your values and priorities. Is the extra space truly worth the financial drain? Could downsizing help you strike a better balance between enjoying life and building wealth? Remember, you only have one life—don’t waste it paying for things you don’t need. Make your money work for you, not against you.

Cheers

Andy

Valencia

Huge thanks to my girlfriend for taking this stunner! We love Valencia!

Sources:

House Usage Study

https://thinksaveretire.com/think-you-need-a-2000-sqft-house-to-be-comfortable-think-again/

2. United States

– Average house size: U.S. Census Bureau, Characteristics of New Housing.

– Occupancy rates: Pew Research Center, Household Composition Trends.

– Median house price: Zillow, U.S. Housing Market Overview

3. Australia

– Average house size: Australian Bureau of Statistics, Building Approvals Data.

– Occupancy rates: Australian Institute of Family Studies, Household Size Statistics.

– Median house price: CoreLogic, Monthly Housing Market Update.

4. United Kingdom

– Average house size: UK Government, English Housing Survey.

– Occupancy rates: Office for National Statistics (ONS), Housing and Household Data.

– Median house price: HM Land Registry, UK House Price Index.

5. New Zealand

– Average house size: Statistics New Zealand, Building Consents Issued Data.

– Occupancy rates: New Zealand Ministry of Housing and Urban Development, Household Statistics.

– Median house price: Real Estate Institute of New Zealand (REINZ), Monthly Property Report.

6. Investment Data

– ETF performance: Vanguard Australia, VAS ETF Historical Returns.