Every financial decision you make comes with a hidden price tag—one that isn’t always obvious at first glance. This hidden cost is known as opportunity cost, and it can have a massive impact on your long-term wealth. Whether it’s choosing between buying a new car or investing that money, or opting for a bigger house when a smaller one would do, every choice means giving up an alternative that could have led to greater financial freedom. Understanding this concept can be the difference between simply making ends meet and building life-changing wealth.

Opportunity Cost

Opportunity cost is the value of the next best alternative that is forgone when making a decision. It represents the benefits or potential gains that are sacrificed by choosing one option over another. In a nutshell, Opportunity Cost is what you give up when you choose something else.

The True Cost of Buying a New Car

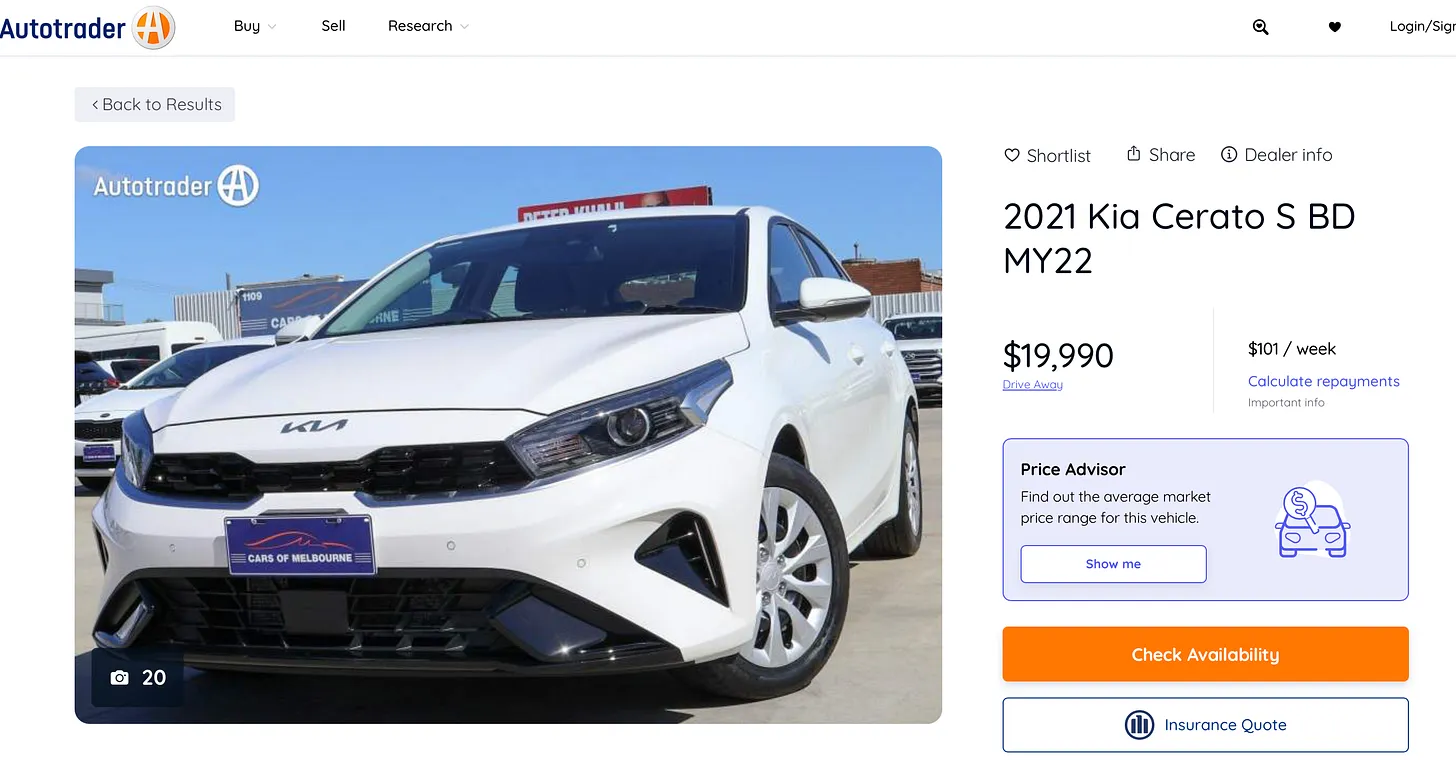

Let’s say you have $50,000 to either buy a nice car or invest the money.

Option 1: Buy the Brand-New Car

You purchase a brand-new car for $50,000.

- After 5 years, the car depreciates and is now worth only $20,000.

- You’ve lost $30,000 in depreciation, plus you had to pay for maintenance, insurance, and fuel along the way. Yikes!

Alternative: Buy a Quality Used Car & Invest the Rest

Instead, you buy a reliable second-hand car for $20,000 and invest the remaining $30,000 in an index fund earning an average 8% return per year.

- After 5 years, your used car is now worth around $10,000 (assuming a more modest depreciation).

- Your $30,000 investment grows to about $44,100. Ka-ching!

Opportunity Cost Breakdown

By buying the brand-new car, you missed out on the chance to have an extra $24,100 from the money you could have invested over 5 years.

Instead of losing $30,000 on a new car, you could have bought a reliable used car and still had over $44,000 growing in your investment account. This extra money would help you build more wealth over time.

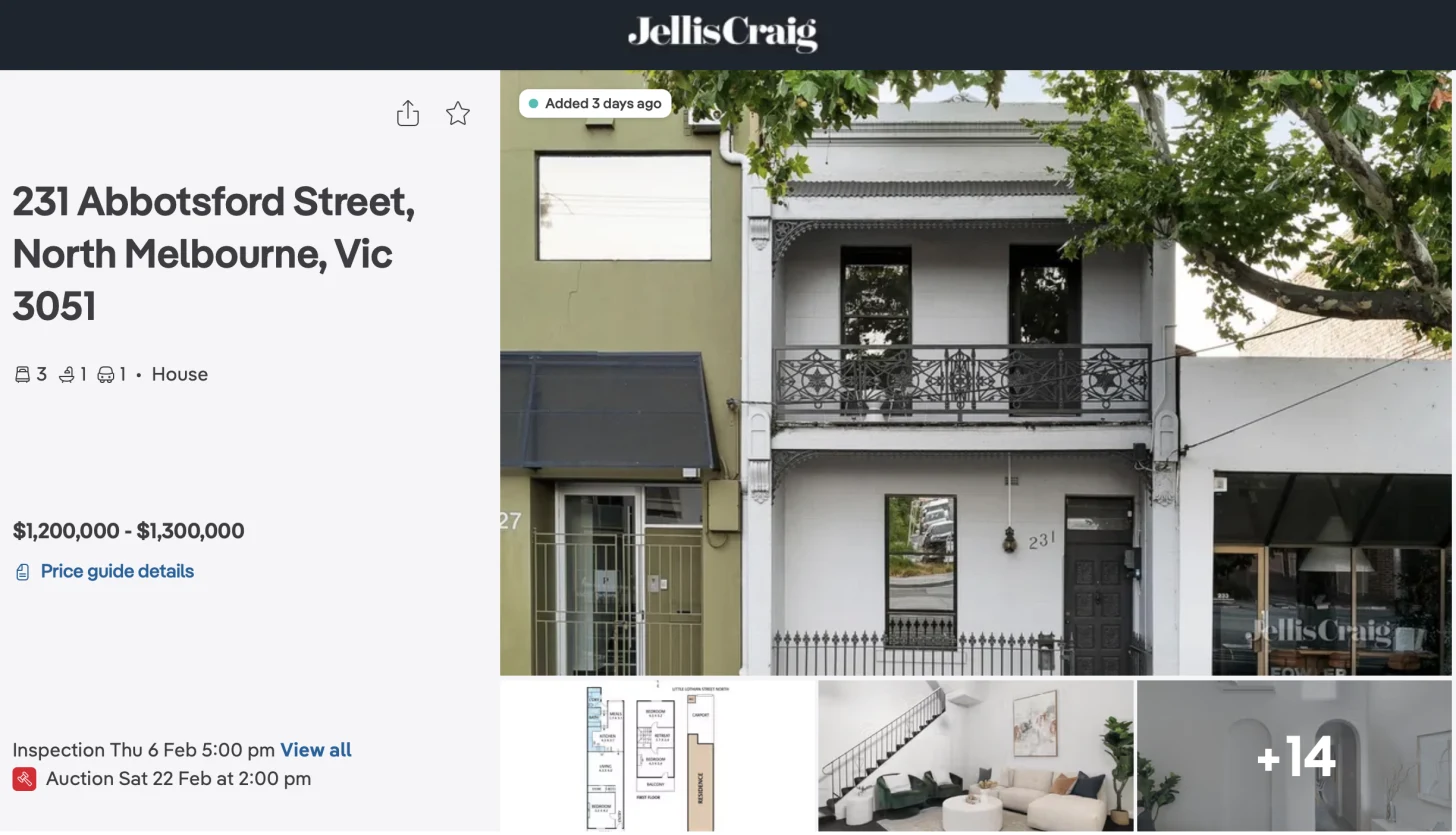

The Opportunity Cost of Buying a Bigger House

Sarah and Brent, from good ol’ Melbourne, Australia, are looking to buy a house. They don’t have children, but a couple of times a year, Brent’s mum stays for a week while visiting. With this in mind, they decide to spend $1,300,000 on a home, thinking the extra space will be useful. You know, for parties and entertaining and such.

However, after a year, they realise they only use 40% of the house—just the bedroom, kitchen, and living room. The extra guest rooms and small backyard mostly go unused. This is very common isn’t developed countries.

Mortgage Breakdown – Bigger House ($1,300,000)

- Deposit (20%): $260,000

- Loan Amount: $1,040,000

- Average Interest Rate: 7% over 30 years (Safe)

- Monthly Repayment: ~$6,930

- Total Paid Over 30 Years: ~$2,495,000

Alternative – Smaller Town House ($790,000)

Instead, Sarah and Brent could have bought a smaller townhouse for $790,000, which would still meet all their needs and allow Brents Mum to stay.

Mortgage Breakdown – Smaller House ($790,000)

- Deposit (20%): $158,000

- Loan Amount: $632,000

- Average Interest Rate: 7% over 30 years (safe)

- Monthly Repayment: ~$4,210

- Total Paid Over 30 Years: ~$1,515,000

Opportunity Cost Over 25 Years

By choosing the bigger house, they:

- Upfront Deposit Difference: Paid $102,000 more in the initial deposit ($260,000 vs. $158,000). If they had invested this difference in the Vanguard Australian Shares Index ETF (VAS), which has an average annual return of approximately 8.28%, over 25 years, it could have grown to about $698,500.

- Monthly Repayment Difference: Paid an additional $2,720 per month in mortgage repayments. If they had invested this monthly difference in VAS at the same average annual return, over 25 years, it could have accumulated to approximately $2,488,000.

- Total Potential Investment Growth: Combining both the upfront deposit and the monthly repayment differences, they could have amassed around $3,186,500 over 25 years by opting for the smaller house and investing the savings in VAS.

Lesson

Their decision to buy a larger house didn’t just cost them $510,000 more upfront—it also cost them the opportunity to build nearly $3.2 million in extra wealth by investing the difference in VAS. By choosing the smaller home, they could have secured a comfortable place to live, significantly accelerated their path to early retirement, and enjoyed greater financial freedom.

Conclusion

At its core, opportunity cost isn’t just about money—it’s about maximizing your choices to align with your long-term goals. A flashy car or a spacious house might bring short-term satisfaction, but the real question is: what are you sacrificing in the process? By thinking critically about opportunity cost, you can make smarter financial decisions that allow you to build wealth, retire earlier, and create the life you truly want. The next time you’re faced with a big purchase, ask yourself: Is this really worth what I’m giving up?

Cheers

Andy

Panama City.. for now

Morning coffee with a view

Sources:

https://www.realestate.com.au/news/melbourne-predicted-to-almost-be-1m-housing-city-again-by-2026-kpmg-house-price-forecast/

https://www.canstar.com.au/home-loans/average-interest-rates-home-loans/

https://www.morningstar.com/etfs/xasx/vas/performance